Interdependence and Industrial Capacity: Southeast Asia’s Energy Transition in a China-Centered Clean Energy Ecosystem

Kevin Zongzhe Li

Kevin Zongzhe Li is a Fellow at the Asia Society Policy Institute's Center for China Analysis.

June 22, 2026

Introduction

Across Asia, the energy transition has become a climate challenge, an industrial race, and a geopolitical problem all at once.

China sits at the center of the global clean energy ecosystem across manufacturing, mineral processing, and finance. Over the past decade, Chinese scale has helped drive roughly 80% declines in solar photovoltaic (PV) costs and 60% declines in onshore wind costs.[1] In 2024, China accounted for over half of global wind and solar additions and manufactured more than 70% of the world’s electric vehicles (EVs).[2][3] Its Fifteenth Five-Year Plan further consolidates ambitions to deepen clean energy manufacturing dominance, intensifying concerns over global industrial overcapacity.[4]

Southeast Asia, home to nearly 700 million people, is just as consequential. The Association of Southeast Asian Nations (ASEAN) is projected to account for more than a quarter of global energy demand growth through 2035.[5] The region commands a unique position of critical mineral endowments, emerging industrial platforms, and fast-growing power demand with tight fiscal space, persistent energy security concerns, and acute climate exposure.[6] Recent conflict in the Middle East has sharpened these vulnerabilities, exposing how fossil fuel supply shocks and price volatility can spill quickly into power costs, industrial competitiveness, and household welfare. Clean energy is therefore a development strategy, an energy security imperative, and, increasingly, a source of social and political resilience for Southeast Asia.

At a time of renewed energy volatility, durable cooperation in clean energy between China and ASEAN offers one response. Cooperation across in renewables, grids, and clean energy supply chains can reduce exposure to external shocks while deepening economic interdependence.

The core question is this: can Southeast Asia turn cooperation with China’s clean energy ecosystem into durable local capability, or will that entrench dependency?

Indeed, clean technologies no longer move through global markets according to efficiency and scale alone. Southeast Asia now has to work through two forces at the same time: China’s supply-side scale in manufacturing and processing, and its own demand growth, resource endowments, and policy constraints – within which Western market access and trade compliance impose additional pressure. The challenge lies in navigating these complex interactions.

In many parts of Southeast Asia, Chinese capital underwrites both renewables and coal-linked industrial expansion – accelerating decarbonization while reinforcing fossil fuel lock-in. Recognizing that clean energy is set to expand rapidly in Southeast Asia, what remains uncertain is the distribution of its benefits and risks.[7]

This brief asks three questions:

- What do zero-sum and positive-sum outcomes look like in a China-centered ecosystem?

- Where do leverage points emerge as cooperation expands?

- What institutional conditions allow Southeast Asia to build durable industrial capability?

To answer them, the brief argues that China and Southeast Asia have real complementarities across four modes of clean energy engagement: trade in finished clean energy goods, localized manufacturing, infrastructure, and extractives and processing.

Across these modes, outcomes depend, importantly, on how institutional engagement is carried out through the life cycle. In particular, three variables recur: control over market access and licensing, the conversion of production and infrastructure into domestic capability, and enforcement and governance after projects begin.

Two possible futures of China-Southeast Asia cooperation

This brief sets out two possible futures for Southeast Asia under a China-Southeast Asia clean energy partnership.

In a zero-sum transition, Southeast Asia functions primarily as a consumption market, assembly node, and source of raw materials. Higher-value manufacturing, advanced processing, and ultimate decision-making remain elsewhere. Clean energy deployment still advances, albeit at a slower pace with deeper reliance on Chinese capital, technology, and supply chains.

In a durable green industrial future, China invests more extensively in Southeast Asian manufacturing while regional governments strengthen domestic institutions, enforce standards, and coordinate industrial policy. Clean energy deployment then supports local upgrading, regional integration, and stronger bargaining power within the China-centered clean energy ecosystem.

Comparative leverage in China-Southeast Asia cooperation

In China-Southeast Asia clean energy cooperation, control over market access, mineral endowments, export outlets, licensing authority, and strategic infrastructure made up a suite of leverage. These sources of leverage, however, are unevenly distributed across countries.

Indonesia’s nickel endowment gives it influence over the EV battery supply chain. Vietnam and Thailand derive leverage from export-oriented manufacturing ecosystems and larger labor pools, while Vietnam’s rare earth reserves could give it partial Indonesia-like characteristics in some future scenarios.[8] Malaysia and Singapore function as regulatory, logistical, and financial nodes. Countries positioned along emerging cross-border electricity corridors, including the Laos-Thailand-Malaysia-Singapore interconnection, can strengthen regional energy resilience. These differences mean that Southeast Asia does not, and should not be expected to, act as a single bloc, but as a set of economies with distinct positions across the value chain.

China’s clean energy system is powerful, but is also not fully self-reliant. The current expansion of manufacturing and processing capacity under the Fifteenth Five-Year Plan depends on two factors outside China’s control: reliable access to imports and access to markets, both of which lie partly outside Beijing’s control. On imports, China refines and manufactures at scale, but many of the underlying resources are located abroad. Nickel processing requires Indonesian mining output. Terbium and dysprosium from Myanmar affect feedstock availability. These supply relationships create bargaining power for Southeast Asian governments.

Southeast Asia also gains leverage from rising demand. As trade enforcement tightens in the US and Europe, Chinese firms have stronger incentives to seek markets where clean energy deployment can still grow quickly. Southeast Asia is one of those regions. It offers Chinese firms a growing market for clean energy goods, and possible production sites.

Importantly, leverage is relational rather than absolute. Southeast Asia’s own clean energy growth depends on access to goods, technology, capital, and, eventually, demand for its manufactured exports. The relationship is, therefore, one of interdependence.

Four Modes of Engagement

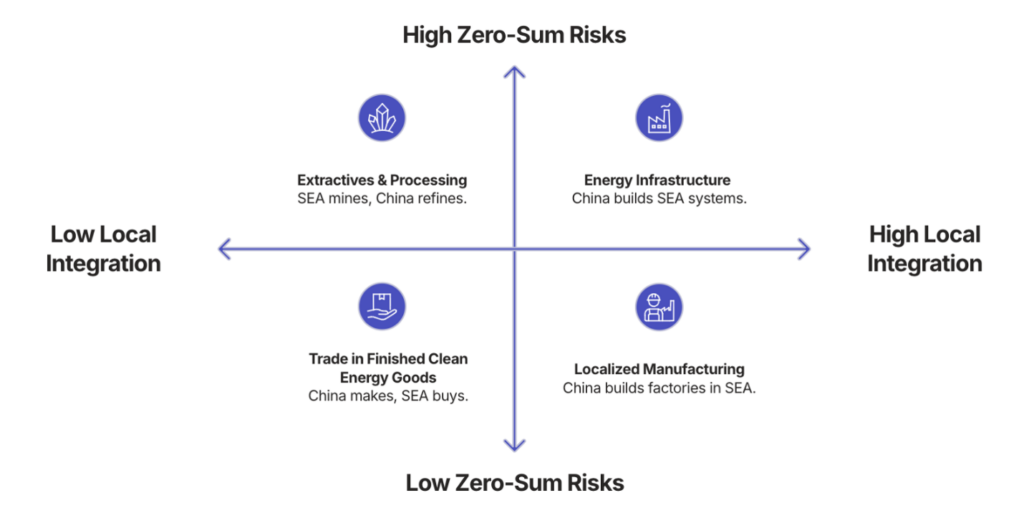

Zero-sum risks and positive-sum opportunities differ across four distinct modes of engagement: 1) trade in finished clean energy goods, 2) localized manufacturing, 3) energy infrastructure, 4) extractives and processing. Treating clean energy as a single category obscures where the real vulnerabilities and opportunities lie.

The figure above maps them along two dimensions: the degree of local economic integration (x-axis) and the intensity of zero-sum risk (y-axis). . Localized manufacturing embeds capital and labor domestically, raising integration but not necessarily systemic risk. Energy infrastructure combines deep local integration with long-term fiscal, technical, and political exposure. Extractives and processing, by contrast, often create fewer local linkages while concentrating high environmental and geopolitical risk. In practice, however, these modes can overlap; where trade involves ores, processed minerals, or battery inputs, it moves closer to extractives and processing and carries, understandably, a different risk profile.

These differences also influence when leverage has force. Instruments that are effective at entry – such as market access conditions or investment approvals – lose power once assets are built or supply chains are in place. At that point, governments face fewer options and higher costs, should they wish for a course change. Late-stage interventions can still be pursued through licensing, regulation, or legal action, but they tend to be more disruptive, commercially or politically. Timing therefore carries as much weight as the policy choices themselves.

1. Trade in Finished Clean Energy Goods

Globally, China recorded a trade surplus of roughly US$1.2 trillion in 2025, with exports rising 5.5% despite intensified tariff pressure.[9] Trade with ASEAN expanded 7.4% year-on-year, alongside the China-ASEAN Free Trade Area (CAFTA) 3.0 Upgrade Protocol, signed in October 2025. Clean energy exports accounted for a growing share of this expansion.[10]

Although only one in five of China’s EVs was exported in 2025 (around 3.4 million units), EV exports surged 86% year-on-year.[11] Battery and solar exports also expanded sharply, underscoring the scale of outward pressure from China’s clean technology industries. Southeast Asia absorbed part of this surge, with Chinese EV shipments to the region nearly doubling over the year and monthly shipments exceeding 50,000 vehicles at the peak.[12]

Against this backdrop, trade in solar PV modules, batteries, EVs, and power equipment carries low structural zero-sum risk. Imports do not necessarily create sovereign liabilities, immobile assets, or site-specific ecological risk. Unlike infrastructure finance, trade is reversible and price-mediated, and governments retain some degree of policy autonomy via instruments for adjusting exposure. For Southeast Asia, competitively priced clean technologies have substantively lowered system costs and accelerated deployment as electricity demand expands.

The risk, instead, lies less in trade itself than in trade governance.

Market outcomes already vary across the region. In Singapore, Chinese EV brands rapidly gained share in 2025 as consumers responded to growing price affordability, pushing adoption to record levels.[13] In Thailand, intensified competition has squeezed Japanese automakers and parts suppliers, placing legacy supply chains under strain. Trade produces consumer gains alongside industrial displacement.[14]

Indeed, similar dynamics have appeared in other sectors, where inflows of low-cost Chinese goods, such as garments and textiles, have led to firm closures, workforce displacement, and varying degrees of public discontent.[15] These pressures can lead to protectionist measures, which, if extended to clean energy imports, can slow deployment and undermine climate goals.

Yet scale does not equal autonomy. China’s manufacturing base depends on conditions it does not fully control. Amid domestic overcapacity, deflation, and price competition – pressures Beijing has acknowledged yet struggled to contain – manufacturers increasingly rely on overseas markets.[16] As advanced economies including the US and EU tighten trade enforcement, Southeast Asia’s expanding middle class markets become commercially consequential. Such commercial dependence creates incentives for Beijing to preserve market access and strive for regulatory predictability in the region.

In trade, vulnerabilities arise mainly from weak governance and reactive politics. The issue is therefore not dependence through imports, but the terms under which market access is governed, and whether governments retain the ability to recalibrate exposure constantly, if need, as domestic conditions evolve.

2. Localized Manufacturing

Localized manufacturing offers Southeast Asia its clearest route to value capture in the energy transition. More than trade in finished goods, manufacturing brings capital, workers, and suppliers into host economies. For governments pursuing the daunting agenda of both decarbonization and industrial upgrading, clean energy investment serves both.[17]

The scale is significant. ASEAN has consistently been the primary destination for Chinese overseas green manufacturing projects, with planned investment reaching US$17 billion in 2024.[18] Indonesia’s EV battery ecosystem, developed around its nickel industry and downstreaming policies, has attracted major Chinese firms such as Tsingshan and Huayou Cobalt. Malaysia has positioned itself within solar and battery supply chains, linking investment to workforce development and regional integration.[19] Capital inflows have been substantial.

Most notably, enclave industrialization is a major risk. In many cases, production facilities may be physically located in Southeast Asia, but weakly connected to domestic ecosystems. High-value segments – including advanced materials, cell design, and system integration – often remain beyond reach. Intermediate inputs are imported, technical management foreign-led, and domestic firms confined to lower-tier subcontracting. In this scenario, capability does not grow in parallel.

Employment metrics further obscure this dynamic. Evidence from Malaysia suggests that certain forms of foreign direct investment generate limited wage spillovers relative to output growth. Manufacturing becomes politically visible, but economically thin.[20]

External trade enforcement adds further vulnerability. Many ASEAN facilities are export-oriented, particularly toward the US and EU. When rules of origin tighten or tariffs escalate, commercial viability can shift abruptly. In 2025, the US imposed duties of up to 3,521% on solar imports from several ASEAN countries, along with a 40% tariff on goods identified as transshipments through Vietnam.[21][22] Production networks financed by Chinese capital or reliant on Chinese inputs are directly exposed. Manufacturing leverage requires cost competitiveness and preserving export eligibility through compliance.

Often overlooked, Southeast Asian governments actually possess greater leverage in manufacturing than trade. Investment approvals, tax incentives, land allocation, electricity pricing, and licensing are, typical, firmly within domestic control. On the flip side, China’s leverage in manufacturing operates less through state direction than through commercial imperatives – such as margin pressure and intense domestic competition. Overseas production helps absorb excess capacity and mitigate trade risk, but success depends on navigating host-country politics, reputational legitimacy, and access to Western markets. Stability and regulatory predictability in Southeast Asia are therefore commercially valuable.

Localized manufacturing is the hinge, and indeed the strongest bridge, between clean energy deployment and industrial development, if pursued with a strong focus on building the depth of capacity and integration.

3. Energy Infrastructure

Energy infrastructure is the backbone of the energy transition. Unlike trade or manufacturing, generation capacity, transmission networks, storage systems, and EV charging are long-lived, capital-intensive assets lock in fiscal exposure and political coalitions for decades.

Where Southeast Asian governments possess leverage in this domain is, in principle, significant and at the entry point. Public authorities control procurement processes, tariff approvals, grid planning, land acquisition, and regulatory oversight. They determine whether contracts are competitively tendered or directly negotiated. They choose between public utilities or private concessions. They also influence the pace at which renewables and storage enter grid systems.

Yet this leverage is only as strong as institutional credibility.

China plays a major role in regional infrastructure finance and construction. Chinese policy banks and engineering firms have financed and built hydropower projects in Laos, coal plants in Vietnam during the peak Belt and Road Initiative (BRI) years, and solar parks in Thailand.[23][24][25] In Laos, majority control of the national transmission grid was transferred to China Southern Power Grid under a 25-year concession arrangement. Driven by mounting debt and infrastructure financing needs, the arrangement illustrates how infrastructure ownership changes hand under sovereign fiscal pressure.

In Indonesia, captive coal plants for nickel refining at industrial parks such as Morowali reveal a different tension.[26] These critical facilities power the global EV battery supply chains, yet are hardly “green” industrialization. As renewable capacity expands, fossil fuel persists alongside it. Infrastructure accelerates decarbonization in one segment, and spikes emissions in another.

At the same time, Chinese firms such as Trina Solar, BYD, Huawei, and CATL supply large-scale solar and storage systems across ASEAN, contributing to renewable buildout. Project design and system integration determine the direction of impact more than the origin of capital alone.

China’s position in infrastructure has evolved with its outbound financing model. Overseas lending has moderated relative to peak BRI volumes. Policy banks now price sovereign risk more cautiously, and project bankability and reputational exposure carry greater weight than during the first wave of outbound expansion. Stability and regulatory predictability in host countries have become commercial prerequisites. The evolving “BRI 2.0” emphasizes greener and smaller-scale (“small and beautiful 小而美”) projects.[27]

The main risk is not foreign financing per se, but misaligned incentives and rigid contracts. Hydropower development along the Mekong in Laos and Cambodia shows how ecological and cross-jurisdictional externalities generate political friction long after construction.[28] Stalled Western-led efforts to accelerate coal retirement, such as the Just Energy Transition Partnership’s financing for early retirement of Indonesia’s Cirebon-1 plant, show how technically viable transitions can be complicated by entrenched political interests.[29]

Positive-sum outcomes require clean rules before construction begins: competitive tendering, publication of key contractual terms, independent regulatory oversight, and alignment with long-term grid planning. Regional integration initiatives such as the ASEAN Power Grid, including the Lao PDR-Thailand-Malaysia-Singapore Power Integration Project, diversify supply sources and increase system flexibility.[30] Cross-border interconnections expand policy options when they are planned through multilateral frameworks.

Concepts such as zero-carbon industrial parks – already under construction in parts of China – are potentially next frontiers. Southeast Asian economies, including Indonesia, have expressed interest in replicating such models.[31]

The time dimension in infrastructure is unforgiving. Leverage is strongest before contracts are signed and assets are built. Decisions made today define fiscal and emissions trajectories for decades and policy flexibility narrows considerably. Infrastructure missteps will not be easily unwound and require the greatest degree of institutional seriousness.

4. Extractives and Processing

Extractives and processing are the weakest and most fragile segment of Southeast Asia’s clean energy engagement. Electrification depends on secure access to nickel, rare earth elements, lithium, cobalt, and graphite. This segment involves immobile resources, concentrated rents, environmental risk, and political contestation. Once mines, processing sites, and supply relationships are in place, ecological and geopolitical dependencies become difficult to unwind.

Southeast Asia possesses meaningful, if not significant, upstream leverage. Indonesia is the world’s largest nickel producer.[32] Myanmar has supplied a substantial share of China’s heavy rare earth imports.[33] Malaysia eagerly positions itself within rare earth processing and separation, after its raw rare earths export ban.[34] Vietnam boosts substantive rare earth deposit. Control over deposits, licensing, and export regimes gives ASEAN governments true bargaining power.

Yet upstream leverage often fails to produce downstream value capture. The risk in this mode is more acute than in others.

In nickel, Chinese firms have developed large-scale refining and industrial parks in Morowali and Weda Bay. These investments have accelerated Indonesia’s integration into global EV supply chains and generated significant revenue and employment. At the same time, deforestation, waste disposal, worker safety, and refining concentration raise hard questions about local value retention and environmental liability. Recent production quotas and regulatory adjustments reflect Jakarta’s efforts to regain control.[35]

Myanmar presents a more acute illustration of fragility. Heavy rare earth extraction has been concentrated in conflict-affected regions with limited environmental oversight and complex local intermediaries. Disruptions to mining areas have exposed how local security dynamics quickly reverberate through global supply chains.[36] In such contexts, extraction is entangled with governance vacuums and conflict financing.

Malaysia occupies a different but delicate position. As it expands rare earth processing while maintaining ties with both China and Western partners, it navigates intensifying geopolitical competition over supply chain control. Processing depth creates opportunity, but it also increases exposure to strategic pressure as advanced economies link mineral supply chains to national security.[37]

China’s dominance in refining will remain a defining feature for decades. In several critical minerals, it controls the majority of global processing capacity, giving it pricing influence and supply chain leverage.[38] That dominance, however, is not absolute. China relies on overseas upstream resources, and its projects remain subject to host-country regulation, political instability, and rising international scrutiny of environmental and transparency standards. Parallel efforts by advanced economies to construct alternative supply chains introduce longer-term competitive pressure.[39]

The core risk in extractives is indeed governance failure. Where licensing is opaque, environmental safeguards are weak, and fiscal regimes poorly structured, extraction becomes enclave-driven: raw materials flow outward while pollution and displacement stay local.

Positive-sum outcomes thus require deliberate linkage between extraction and industrial depth. Efforts including transparent licensing, enforceable environmental standards, credible monitoring, and sound revenue management are prerequisites. Downstream integration into refining, precursor materials, or battery components must be pursued strategically. When governance capacity is weak, exercising restraint (as opposed to rapid scaling) may serve nations better.

Extractives are a stress test. They offer the most visible leverage, control over scarce inputs, but also the highest liability. Environmental damage is costly to remediate. Industrial concentration, once entrenched, is difficult to rebalance. The time horizon in extractives is long and unforgiving.

Conclusion: Southeast Asia’s Choice and Opportunity

Taken together, these four modes point to a single lesson: positive and durable outcomes require sustained institutional control across project lifecycles. Governments gain the most when they retain influence over entry, enforce standards during operation, and link China engagement to broader industrial strategies. Where these conditions are absent, zero-sum outcomes become more likely.

Southeast Asia’s energy transition will be defined not only by the scale of renewable deployment. Engagement with China is structurally unavoidable, but if China and Southeast Asia can chart clear frameworks and guardrails, clean energy transition can move along in a durable manner.

Clean energy cooperation between China and Southeast Asia carries consequences for regional stability. It can support Southeast Asia’s industrial development or reinforce its position at the lower end of global value chains. At this juncture, the difference lies in to what degree governments retain policy autonomy as cooperation deepens, using well-timed leverage to exercise power effectively.

References

[1] Zheng Xin, “China’s tech cutting cost of renewables,” China Daily, October 25, 2025, https://www.chinadaily.com.cn/a/202510/25/WS68fc0d7da310f735438b6dac.html.

[2] Ma Li and Charles Bourgault, “China’s renewable energy boom has its own challenges. Here’s what we can learn,” World Economic Forum, December 3, 2025, https://www.weforum.org/stories/2025/12/china-adding-more-renewables-to-grid/.

[3] Global EV Outlook 2025: Expanding sales in diverse markets, International Energy Agency, May 14, 2025, https://www.iea.org/reports/global-ev-outlook-2025/.

[4] “中共中央关于制定国民经济和社会发展第十五个五年规划的建议,” Ministry of Commerce of the People’s Republic of China, 2025, https://www.mofcom.gov.cn/syxwfb/art/2025/art_d5da513be3fe491582dd17eae6d805d9.html.

[5] Southeast Asia Energy Outlook 2024: Executive Summary, International Energy Agency, 2024, https://www.iea.org/reports/southeast-asia-energy-outlook-2024/executive-summary.

[6] “Climate Change Vulnerabilities, Social Impacts, and Education for Autonomous Adaptation,” Economic Research Institute for ASEAN and East Asia, n.d., https://www.eria.org/research/climate-change-vulnerabilities--social-impacts--and-education-for-autonomous-adaptation.

[7] “Southeast Asia’s role in the global energy system is set to grow strongly over next decade,” International Energy Agency, October 21, 2024, https://www.iea.org/news/southeast-asias-role-in-the-global-energy-system-is-set-to-grow-strongly-over-next-decade.

[8] Shelby N. Johnston, “Rare Earths,” U.S. Geological Survey, 2026, https://pubs.usgs.gov/periodicals/mcs2026/mcs2026-rare-earths.pdf.

[9] Joe Cash and Xiuhao Chen, “China’s trade ends 2025 with record $1.2 trillion surplus despite Trump tariff jolt,” Reuters, January 14, 2026, https://www.reuters.com/world/china/chinas-trade-ends-2025-with-record-trillion-dollar-surplus-despite-trump-tariffs-2026-01-14/.

[10] Fajar Hirawan, “China-ASEAN economic cooperation to strengthen trade, value chains in 2026,” Global Times, January 18, 2026, https://www.globaltimes.cn/page/202601/1353560.shtml.

[11] Lauri Myllyvirta and Belinda Schaepe, “Analysis: Clean energy drove more than a third of China’s GDP growth in 2025,” Carbon Brief, February 5, 2026, https://www.carbonbrief.org/analysis-clean-energy-drove-more-than-a-third-of-chinas-gdp-growth-in-2025/.

[12] Charles Lester, “Global EV sales reach 20.7 million units in 2025, growing by 20%,” Benchmark Mineral Intelligence, January 14, 2026, https://source.benchmarkminerals.com/article/global-ev-sales-reach-20-7-million-units-in-2025-growing-by-20.

[13] Aqil Hamzah, “Auto brand BYD sells over a fifth of all new cars in S’pore as EV sales hit record high in 2025,” The Straits Times, January 23, 2026, https://www.straitstimes.com/singapore/transport/singapores-top-auto-brand-byd-sells-over-a-fifth-of-all-new-cars-in-2025-as-evs-reach-record-high.

[14] The Japan News, “Japanese automakers losing market share in Southeast Asia amid increased competition from Chinese brands,” The Daily Star, January 7, 2026, https://www.thedailystar.net/business/news/japanese-automakers-losing-market-share-southeast-asia-amid-increased-competition.

[15] Jessica C. Liao and Zenel Garcia, “China Is Squeezing Southeast Asia: As Imbalances Grow, a Backlash Is Brewing,” Foreign Affairs, March 24, 2026, https://www.foreignaffairs.com/china/china-squeezing-southeast-asia.

[16] Amy Hawkins and Helen Davidson, “China warns EV makers to stop price-cutting to protect the economy,” The Guardian, August 5, 2025, https://www.theguardian.com/business/2025/aug/05/china-warns-ev-makers-stop-price-cutting-production-involution.

[17] “RI targets 34 percent renewables in energy mix by end of 2034,” The Jakarta Post, June 4, 2025, https://www.thejakartapost.com/business/2025/06/04/ri-targets-34-percent-renewables-in-energy-mix-by-end-of-2034.html.

[18] Xiaokang Xue and Mathias Larsen, “China’s Green Leap Outward: The rapid scale-up of overseas Chinese clean-tech manufacturing investments,” Net Zero Industrial Policy Lab, September 9, 2025, https://www.netzeropolicylab.com/china-green-leap.

[19] Neo Chee Hua, Tiew Mei Yi, Chin Mui Yin, Foo Lee Peng, Chong Shyue Chuan, Phuah Kit Teng, Sia Bik Kai, Ong Sheue Li, Tey Sheik Kyin, and Wong Tee Hao, “Assessing the Roles of Chinese Enterprises in Malaysia’s Economic Development,” China Enterprises Chamber of Commerce in Malaysia and Southeast Asia Research Centre for Humanities, August 2025, https://ceccm.com.my/wp-content/uploads/2025/08/Watermark_ASSESSING-THE-ROLES-OF-CHINESE-ENTERPRISES-IN-MALAYSIAS-ECONOMIC-DEVELOPMENT_compressed-1.pdf.

[20] Geoffrey Williams, “Is FDI creating expensive low-paid jobs?,” Free Malaysia Today, January 28, 2026, https://www.freemalaysiatoday.com/category/opinion/2026/01/28/is-fdi-creating-expensive-low-paid-jobs.

[21] “US sets tariffs of up to 3,521% on South East Asia solar panels,” BBC News, April 21, 2025, https://www.bbc.com/news/articles/c5ygdv47vlzo.

[22] Vu Nguyen Hanh, “Transshipment and Origin Risks: How Vietnam-Based Businesses Can Stay Compliant,” Vietnam Briefing, October 15, 2025, https://www.vietnam-briefing.com/news/transshipment-origin-risks-vietnam-based-businesses-stay-compliant-2025.html/.

[23] Ma Liwenbo, Liu Xiangchen, and Souksanith Sisoulath, “The Nam Ou River Cascade Hydropower Project: Epitome of China-Laos Friendship,” Ministry of Commerce of the People’s Republic of China, n.d., https://www.mofcom.gov.cn/newarticle/beltandroad/la/enindex.shtml.

[24] “Vinh Tan 1 power plant largest Chinese investment in Vietnam,” Belt and Road Portal, July 17, 2017, https://eng.yidaiyilu.gov.cn/p/20048.html.

[25] Tyler Roney, “China poised for Thailand’s solar move,” Dialogue Earth, July 30, 2021, https://dialogue.earth/en/energy/china-poised-for-thailands-solar-move/#:~:text=The%20hybrid%20solar%2Dhydro%20project,Courtney%20Weatherby%2C%20the%20Stimson%20Centre.

[26] Kelly Sims Gallagher, Rishikesh Bhandary, Easwaran Narassimhan, and Quy Tam Nguyen, “Banking on coal? Drivers of demand for Chinese overseas investments in coal in Bangladesh, India, Indonesia and Vietnam,” Energy Research & Social Science 71 (January 2021): 101827, https://doi.org/10.1016/j.erss.2020.101827.

[27] “Key Pathways on a Green and Low-Carbon BRI,” China Council for International Cooperation on Environment and Development, 2022, https://cciced.eco/research/special-policy-study/sps-6-green-belt-and-road-initiative-bri-and-2030-sdgs/.

[28] Saleh Ahmed and Paige Liquin, “Socio-ecological challenges of hydroelectric dams among ethnic minorities in northern Laos,” Environmental Development 46 (June 2023): 100864, https://www.sciencedirect.com/science/article/abs/pii/S2211464523000647.

[29] Hans Nicholas Jong, “Indonesia backs away from coal exit test case amid financial and political pushback,” Mongabay, January 15, 2026, https://news.mongabay.com/2026/01/indonesia-backs-away-from-coal-exit-test-case-amid-financial-and-political-pushback/.

[30] “ASEAN Power Grid (APG),” ASEAN Centre for Energy, n.d., https://aseanenergy.org/apaec/asean-power-grid-apg.

[31] “The World’s First Net Zero Industrial Park,” Envision Group, n.d., https://www.envision-group.com/case-study/ordos-industrial-park.

[32] Ghee Peh, “Indonesia’s nickel companies: The need for renewable energy amid increasing production,” Institute for Energy Economics and Financial Analysis, October 24, 2024, https://ieefa.org/resources/indonesias-nickel-companies-need-renewable-energy-amid-increasing-production.

[33] Amara Thiha, “Northern Myanmar’s Rare Earths Are Shaping Local Power and Global Competition,” New Security Beat, August 4, 2025, https://www.newsecuritybeat.org/2025/08/northern-myanmars-rare-earths-are-shaping-local-power-and-global-competition/#:~:text=Myanmar%20has%20become%20China's%20most,by%20the%20end%20of%202024.

[34] Iman Muttaqin Yusof, “Malaysia courts US to climb critical minerals value chain while keeping raw export ban,” South China Morning Post, February 11, 2026, https://www.scmp.com/week-asia/economics/article/3343222/malaysia-courts-us-climb-critical-minerals-value-chain-while-keeping-raw-export-ban.

[35] “Indonesia to cut nickel mining quota in 2026,” Argus Media, February 11, 2026, https://www.argusmedia.com/en/news-and-insights/latest-market-news/2787275-indonesia-to-cut-nickel-mining-quota-in-2026.

[36] Dylan Butts, “How war-torn Myanmar plays a critical role in China’s rare earth dominance,” CNBC, June 24, 2025, https://www.cnbc.com/2025/06/24/chinas-rare-earth-dominance-myanmar-plays-a-critical-role-.html.

[37] Iman Muttaqin Yusof, “Malaysia courts US to climb critical minerals value chain while keeping raw export ban,” South China Morning Post, February 11, 2026, https://www.scmp.com/week-asia/economics/article/3343222/malaysia-courts-us-climb-critical-minerals-value-chain-while-keeping-raw-export-ban.

[38] IER, “China Will Remain the World’s Dominant Critical Mineral Processing Supplier Through 2030,” Institute for Energy Research, January 20, 2026, https://www.instituteforenergyresearch.org/international-issues/china-will-remain-the-worlds-dominant-critical-mineral-processing-supplier-through-2030/.

[39] Office of the Spokesperson, “2026 Critical Minerals Ministerial,” U.S. Department of State, February 4, 2026, https://www.state.gov/releases/office-of-the-spokesperson/2026/02/2026-critical-minerals-ministerial.

The views and opinions expressed in this article are those of the author(s) and do not necessarily reflect those of the Asia Research Institute, National University of Singapore.